Number of View: 3611

New Pension scheme (NPS) was given a fresh breather of life with effect from 1 April 2015 when the finance minister gave additional Rs. 50,000 tax rebate on investments being made into NPS. While the air was fresh, it was not fresh enough. Investments into NPS are exempt from tax at the time of investments, they continue to accrue tax free returns till maturity BUT are fully taxable at the time of maturity. In summary, NPS is subject to Exempt-Exempt-Tax (EET). This quite contrary to other investment options available in the markets such as PPF, ELSS mutual funds, PF contributions, etc. where the amount on maturity is tax free in the hands of the investor. Before we further take a dig on why you should not invest in NPS, let us give you a few salient features of the scheme.

New Pension scheme (NPS) was given a fresh breather of life with effect from 1 April 2015 when the finance minister gave additional Rs. 50,000 tax rebate on investments being made into NPS. While the air was fresh, it was not fresh enough. Investments into NPS are exempt from tax at the time of investments, they continue to accrue tax free returns till maturity BUT are fully taxable at the time of maturity. In summary, NPS is subject to Exempt-Exempt-Tax (EET). This quite contrary to other investment options available in the markets such as PPF, ELSS mutual funds, PF contributions, etc. where the amount on maturity is tax free in the hands of the investor. Before we further take a dig on why you should not invest in NPS, let us give you a few salient features of the scheme.

This is the single most important driver for not investing in NPS scheme based upon the current tax laws. In the current form, our tax laws relating to NPS are :

This is the single most important driver for not investing in NPS scheme based upon the current tax laws. In the current form, our tax laws relating to NPS are :

New Pension scheme (NPS) was given a fresh breather of life with effect from 1 April 2015 when the finance minister gave additional Rs. 50,000 tax rebate on investments being made into NPS. While the air was fresh, it was not fresh enough. Investments into NPS are exempt from tax at the time of investments, they continue to accrue tax free returns till maturity BUT are fully taxable at the time of maturity. In summary, NPS is subject to Exempt-Exempt-Tax (EET). This quite contrary to other investment options available in the markets such as PPF, ELSS mutual funds, PF contributions, etc. where the amount on maturity is tax free in the hands of the investor. Before we further take a dig on why you should not invest in NPS, let us give you a few salient features of the scheme.

New Pension scheme (NPS) was given a fresh breather of life with effect from 1 April 2015 when the finance minister gave additional Rs. 50,000 tax rebate on investments being made into NPS. While the air was fresh, it was not fresh enough. Investments into NPS are exempt from tax at the time of investments, they continue to accrue tax free returns till maturity BUT are fully taxable at the time of maturity. In summary, NPS is subject to Exempt-Exempt-Tax (EET). This quite contrary to other investment options available in the markets such as PPF, ELSS mutual funds, PF contributions, etc. where the amount on maturity is tax free in the hands of the investor. Before we further take a dig on why you should not invest in NPS, let us give you a few salient features of the scheme.- Minimum yearly contribution is Rs. 6,000

- You are required to invest till retirement or death. Stringent clauses on withdrawal before retirement / death, i.e. a long lock-in period.

- Exemption for contribution upto Rs. 1.5 lac in 80C.

- Additional exemption of Rs. 50K under section 80CCD with effect from 1 April 2015. This gives you a total tax rebate of Rs. 2 lacs. But hold on to your desire to invest in this product till you go through the entire article.

- On maturity, minimum 40% has to be invested in the form of a life annuity, i.e. it wont be available in lump sum but will be invested in an annuity scheme which will provide a regular (e.g. Monthly, quarterly, yearly) income till the death of the annuitant. This is similar to monthly interest paid out of a fixed deposit investment. The annuity can be purchased for upto 80% of the corpus. While the investment into the annuity is not taxable, the regular income out of annuity is taxable.

- Withdrawal of remaining lump sum amount is taxable.

- NPS gives three options to invest your funds in. One of the option is into Equity which invests in index stocks. Not more than 50% can be invested in Equity funds. Other two options are primarily debt options to invest into bonds.

A deeper dig : NPS Taxation – Exempt Exempt Tax

This is the single most important driver for not investing in NPS scheme based upon the current tax laws. In the current form, our tax laws relating to NPS are :

This is the single most important driver for not investing in NPS scheme based upon the current tax laws. In the current form, our tax laws relating to NPS are :- Investment upto Rs. 2 lacs will be considered as a rebate under section 80C and 80CCD. Hence for people in 30% tax slab, their current saving will look like 30% of Rs. 2 lacs = Rs. 60K per year. For many, 80C related deduction tends to get fulfilled by their existing ELSS investments, PF contributions, home loan principal repayments, etc. The more pertinent discussion starts around additional 50K deduction introduced for NPS from 2015 which if not invested, it lapses.

- Once invested, on retirement you have two options :

- Take a larger corpus out in your hands upto a max of 60% – taxed flat as per your tax slab.

- Remaining amount (minimum 40% and maximum up to 80%) needs to be invested in an annuity scheme giving a return of not more than 7% per year (by current standards). By definition, you will not be able to encash an annuity scheme.

We ran a simulation assuming a person John of age 35 years invests Rs. 50,000 per year into NPS for next 25 years with following allocation :

- Maximum possible allocation towards equity funds, i.e. 50%

- Remaining allocation towards bond funds.

- The tax saving on Rs. 50K @ 30% is Rs. 15,000 per year. John invests this amount of Rs. 15,000 per year via SIP into a large cap fund yielding an assumed rate of 15% return over the period of 25 years.

The consolidated return from NPS over the duration of 25 years is assumed to be approximately 12% based upon equity fund yielding a compounding return of 15% and bond fund giving 9%. After 25 years, the value of NPS and Mutual fund investments of Rs. 15K per year would be :

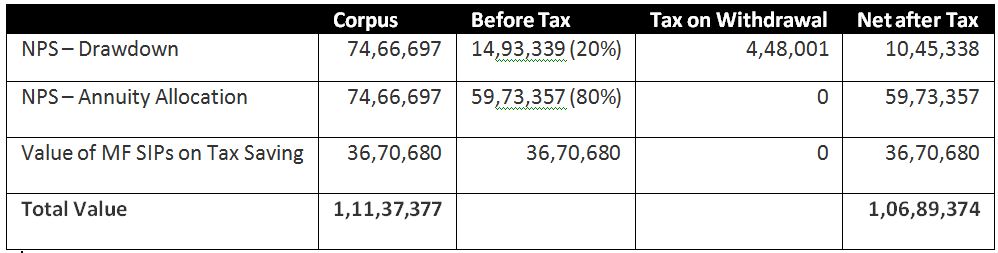

- Total value of amount invested in NPS = 74,66,697

- Total value of tax saving invested in Mutual Fund SIPs = 36,70,680.

- Total Value of corpus = Rs. 1,11,37,376

John has 3 scenarios with him at the end of 25 years.

Scenario A : On maturity, John chooses to draw down minimum possible lump sum amount of 20% and invest the balance 80% into an annuity scheme. Since on withdrawal, NPS is taxable, the net returns in hands of John will be :

Scenario B : On maturity, the John chooses to draw down 50% and invest the balance into an annuity scheme. Net returns in hands of John will be :

Scenario C : John chooses not to invest in NPS. Alternatively he invested Rs. 50,000 per year into a large cap mutual fund yielding similar returns of 15% as assumed in above two scenarios. He does not enjoy immediate 30% tax saving like NPS. The value of the investments after 25 years would be Rs. 1,22,35,600.

Summary of all three scenarios is below for easy reference. You may note without choosing to invest in a NPS, a person can make more wealth. This table does not take into consideration tax impact on the monthly annuity amount which would further drag the returns of NPS.

Still, Top 5 Arguments in favour of NPS and our responses are below

1. It locks my investments till retirement giving me no option and motivation to liquidate prior to retirement.

Well, the cost of giving you a discipline of not being able to sell is whopping over Rs. 20 lacs.

2. When I invest, I get tax rebate .

NPS is classified as Exempt Exempt Tax (EET). What ever tax saving you enjoy while you invest is taken back on withdrawal. The annuity purchased out of the above amounts is also taxable. In summary, it is not a tax efficient investment vehicle.

3. I get to gain from equity investments by investing upto 50% in equity allocation in NPS. This is not available on my PF or PPF investment contributions.

NPS allows maximum allocation of 50% into equities. Even the 50% option is to allocate for a fund which invests in index stocks, i.e. large cap stocks. Large Cap stocks provide lesser returns compared to midcap stocks which are not an option under NPS. Alternatively, if you choose to invest into mutual funds instead of NPS, you have a wide option of investment schemes to suite your risk appetite and can invest upto 100% into Equities across large, midcap, small caps, thematic schemes. This can make a big difference in the overall return compared to the NPS schemes, specially when we are talking about a long term investment horizon of 25 years !

4. NPS is of lower cost compared to other investment funds in the markets

Agreed that NPS could be the cheapest investment option available in the market. Broadly, per transaction cost is 0.25% and a flat annual maintenance cost (AMC) of Rs. 190. This could seem as almost a free AMC cost compared to mutual funds which may charge upto 2.5%. However, the additional returns and flexibility of choosing your allocation which mutual funds give exceeds the charges by several folds.

5. NPS is head ache free. I enroll and forget till retirement.

Again, the cost of your head ache is over Rs. 20 lacs. Alternatively, you could get a financial advisor to help you design and invest in a suitable investment product which could enhance your returns by several folds.

Remember the basics of investing – tax exemption should be a by-product of your investment activity and not the driver of your investments. If it is the latter, it is likely that you may end up in an investment product which will act as a parasite on your wealth for ages !

No comments:

Post a Comment